Net zero roundtables: Plotting a course towards effective portfolio decarbonisation

As a member of the Net Zero Asset Managers Initiative, J.P. Morgan Asset Management has committed to work with our clients on their decarbonisation goals. We brought a network of our clients together, along with a panel of J.P. Morgan Asset Management experts – including climate research analysts, stewardship specialists, and industry analysts – with the aim of identifying the challenges, and the opportunities, created by portfolio decarbonisation. Here, we share some of the key takeaways.

Introduction

As part of our ongoing effort to connect with our clients on topics that are front of mind for them and to help ensure we provide a product offering to help meet their needs, we recently hosted a series of roundtables across Europe to discuss net zero target setting. As a member of the Net Zero Asset Managers Initiative, J.P. Morgan Asset Management has committed to work with our clients on their decarbonisation goals. We brought a network of our clients together, along with a panel of J.P. Morgan Asset Management experts – including climate research analysts, stewardship specialists, and industry analysts – with the aim of identifying the challenges, and the opportunities, created by portfolio decarbonisation. Here, we share some of the key takeaways.

Topic 1 – Evolution of the research agenda

While awareness of the investment implications of climate change has increased since the Paris Agreement in 2015, several common issues remain for the investment industry to assist their clients with their net zero aspirations. One of the biggest issues concerns the shortcomings of existing climate benchmarks, many of which focus on backward-looking emissions data that haven’t evolved to reflect the latest climate research. To enable better manager engagement and performance measurement, investors want climate benchmarks to take a more holistic view of the market by using forward-looking indicators (including science-based targets, green capex and patents), and by including regional perspectives and flexible baselines. However, investors also recognise the challenges faced by index providers and therefore often see the creation of better climate benchmarks as a goal to work towards rather than something that can be addressed immediately.

We acknowledge the challenges that exist when managing dedicated investment portfolios towards addressing the carbon transition. Nevertheless, we aim to address some of these climate benchmark limitations in certain of our own portfolios through integrating insights yielded from our proprietary Carbon Transition Score, which we’ve designed to reach beyond current emissions and science-based targets by assessing companies systematically for transition readiness across more than 15 metrics. In these portfolios, the score may be applied to certain accounts at the company level to help assess progress relative to a sector and/or regional peer group, and to a broad universe to help identify leaders and laggards across an entire market, including through a forward-looking lens.

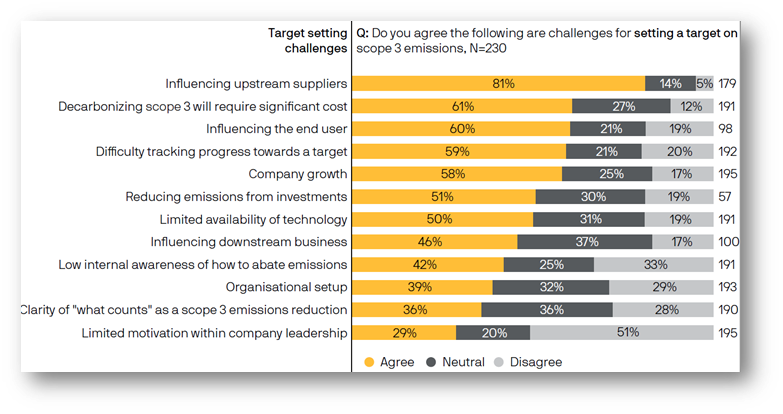

Finally, the enduring challenge of obtaining Scope 3 emissions data is top of mind, given that Scope 3 data can be a useful indicator of the transition risk that a company could be exposed to. Data availability remains a critical roadblock, with companies in many jurisdictions not required to report Scope 3 emissions, including in the US. Companies themselves also face several challenges when setting Scope 3 targets, as noted in a recent survey (see Exhibit 1) by the Science Based Targets initiative (SBTi). While the introduction of corporate disclosure regimes in some regions, notably the European Union (EU), is a positive step, a lack of harmonisation of Scope 3 data requirements looks set to remain an obstacle for the time being.

EXHIBIT 1: CHALLENGES FACED BY COMPANIES WHEN REPORTING SCOPE 3 EMISSIONS

Source: Science Based Targets initiative (SBTi), Catalyzing the Value Chain Decarbonization, Corporate Survey Results, February 2023.

Topic 2 – The importance of investment stewardship

While portfolio decarbonisation could be easily implemented via the exclusion of high emitting sectors or securities, we noted in our discussions that clients are increasingly focused on the decarbonisation of the real economy instead of simply excluding companies from their portfolios. With this in mind, engagement is increasingly in the spotlight, with clients setting engagement targets alongside their decarbonisation goals. This focus on engagement brings requests for greater transparency from asset managers around their own engagement practices and how these engagements are driving portfolio outcomes.

Many of the roundtable attendees also recognised the important role that public policy must play in the net zero transition. In this respect, various stakeholders have different levers they can use to address this issue, while certain asset owners might be better equipped to focus on broader public policy engagement efforts than others. The roundtable attendees also stressed the role of company engagement in understanding if the companies they invest in are undertaking lobbying activities that significantly depart from a company’s decarbonisation claims. Because any misalignment may create material reputational and legal risks to such companies, asset managers – as part of managing risk in their client portfolios – use engagement with such companies concerning the transparency of climate-related lobbying activities, or stated policy positions, and the alignment of these activities with such companies’ decarbonisation claims.

Finally, social factors have a role to play in net zero considerations, with certain clients factoring a just transition into their decarbonisation targets. While social factors can be hard to capture systematically in corporate reporting, we believe engagement to be the best available tool today to help reveal how they are being considered by companies, where relevant, and their potential impact on forward-looking climate-related risk exposures.

Topic 3 – Investment opportunities

Beyond the efforts to assess company transition risk and ascertain credible and meaningful decarbonisation targets for consideration in portfolios with net zero objectives, investors are increasingly optimistic when it comes to the broader investment opportunities that are emerging in response to recent legislation. From policy support, such as the US Inflation Reduction Act and the EU’s Green Deal, to the growing acceptance that investments need to be scaled in areas that can help the world adapt to the negative impacts of climate change, many clients are seeking to increase their allocations to climate solutions.

The potential contribution that alternatives can make to net zero targets is another topic of keen interest, as clients look for assets that can offer both a more direct impact and the potential to generate compelling returns. While data availability and quality has presented a challenge to the use of alternatives, some coalescence around measurement methodologies is now emerging.

Finally, we noted a growing recognition of the opportunities that carbon offsets may provide clients to meet their own net zero targets. However, the timing and the types of offsets to be used remain the subject of discussion. The roundtable attendees see decarbonisation as the primary driver for lowering emissions and therefore want to ensure that offsets are not being used by companies to avoid decarbonising their own operations. Some clients are waiting until 2030 to include offsets in their own targets, as more progress towards decarbonisation should have been achieved by then.

Conclusion

As the prospects of overshooting Paris climate targets become ever more real, clients are increasingly focused on the importance of reaching net zero. While our series of roundtables revealed many of the obstacles that investors face when setting and executing on net zero targets, we remain optimistic that that we can help our clients to achieve their net zero goals via our deep insights and active investment approach. We look forward to continuing to contribute to the industry dialogue and, ultimately, to helping clients reach their individual goals.

NOT FOR RETAIL DISTRIBUTION: This communication has been prepared exclusively for institutional, wholesale, professional clients and qualified investors only, as defined by local laws and regulations.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yield are not a reliable indicator of current and future results. J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://am.jpmorgan.com/global/privacy. This communication is issued by the following entities: In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be; in Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador. In the United Kingdom, by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other European jurisdictions, by JPMorgan Asset Management (Europe) S.à r.l. In Asia Pacific (“APAC”), by the following issuing entities and in the respective jurisdictions in which they are primarily regulated: JPMorgan Asset Management (Asia Pacific) Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, each of which is regulated by the Securities and Futures Commission of Hong Kong; JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), this advertisement or publication has not been reviewed by the Monetary Authority of Singapore; JPMorgan Asset Management (Taiwan) Limited; JPMorgan Asset Management (Japan) Limited, which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Australia, to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Commonwealth), by JPMorgan Asset Management (Australia) Limited (ABN 55143832080) (AFSL 376919). [For all other markets in APAC, to intended recipients only]. For U.S. only: If you are a person with a disability and need additional support in viewing the material, please call us at 1-800-343-1113 for assistance. Copyright 2022 JPMorgan Chase & Co. All rights reserved.